Top 3 Ways Professional Services Organizations Can Exceed Goals in 2022 and Beyond

Discover how successful professional service organizations are finding ways to overcome today’s unique challenges to outpace the competition.

Table of Content

The business landscape is constantly changing and leaders at professional service organizations are facing new challenges in 2022 that pose a direct threat to their business success and profitability. It feels like no matter where you turn, businesses are closing their doors or limiting services due to a variety of reasons. Professional service organizations, including consulting firms, software publishers, and system integrators, are not immune from these impacts. In fact, many are facing shortages of experienced resources, increased competition, and rising overhead.

The most successful professional service organizations are finding ways to overcome today’s unique challenges to outpace the competition and grow profit margin.

Your services are only as good as the resources delivering them. In order to both attract and retain valuable resources, leading Proserv organizations are putting technology in place to streamline processes and increase efficiencies, which in turn increases employee satisfaction and productivity. Eliminating manual processes and tasks eliminates headaches for both your internal team and external constituents.

Ask any billable resource what the biggest area of inefficiency is in their job and the majority will bring up tracking billable hours to jobs or customers. The powerful business applications platform built by Microsoft – Dynamics 365, includes functionality specific to professional services organizations, including a robust time entry user interface.

Within Dynamics 365, your users can easily reduce the amount of time spent tracking billable time with quick keyboard shortcuts that makes entering time and assigning it to a project or customer faster than ever. Shortcuts allow users to add new items, copy rows, edit entries, and more – all with quick key combinations.

No matter where your employees are working – whether that be in the office, at home, or at a customer site, they have the ability to enter time from any browser or mobile device.

Additionally, Dynamics 365 simplifies expense management by allowing users to submit expenses on the same mobile app as they submit time, automatically creating expense lines directly from uploaded receipt images. Automated workflows route time and expense reports to the correct approver for a fast turn around process.

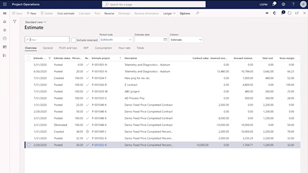

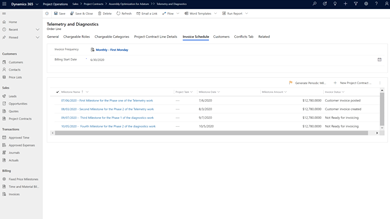

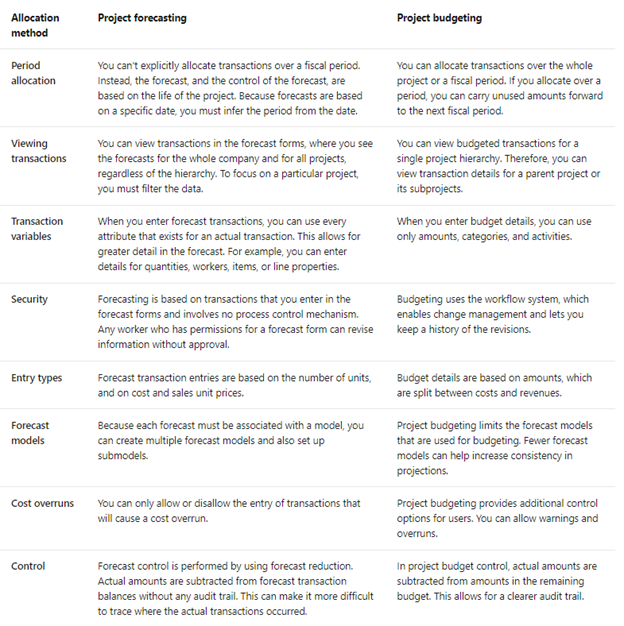

Managing your budget, overall revenue, and cash flow can be complicated. Dynamics 365 allows you to drive your business performance through streamlined project financials.

Dynamics 365 allows you to adhere to accounting standards and practices, including compliance with International Financial Reporting Standards (IFRS).

No matter if you’re focused on closing business and increasing sales, planning upcoming projects, or managing resource utilization, the advanced business intelligence features built into Dynamics 365 and Power BI will help you better understand your current state of business and make the best choices to reach your goals.

Accelerating sales depends on your ability to interact with the right potential customers at the right time. Sales insights uses intelligent pipeline management capabilities and machine learning to direct your sellers time to the best opportunities likely to convert or close as won.

Learn how Velosio can help Professional Service and Project Driven Firms reach their organization goals.

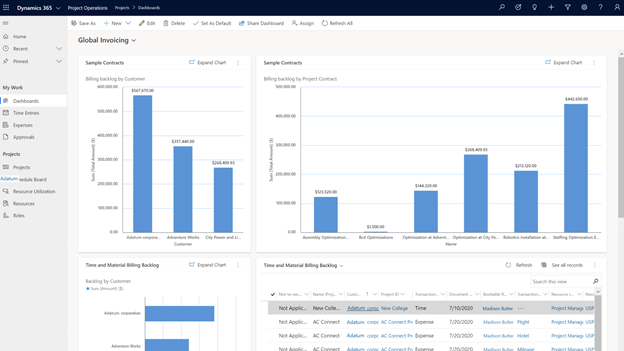

Report on any data within your single platform solution with advanced KPI reporting capabilities, allowing department leaders to understand how they’re stacking up against set goals and historical trends.

Power BI provides graphs and charts to visualize your information, drill down to get additional details, generate reports that include data from a variety of sources, and much more.

Talk to us about how Velosio can help you realize business value faster with end-to-end solutions and cloud services.