SilverLeaf, the leading end-to-end software for cannabis operators.

SilverLeaf, the leading end-to-end software for cannabis operators.

Built on Microsoft Dynamics 365 Business Central, and available on the Microsoft AppSource, SilverLeaf was created to meet the high demand and agile needs of the cannabis market today and drive the requirements for future success in its space.

From Seed to Sale, Tracking and Compliance has Never Been Easier.

Complete business management solution for Cannabis Growers and Processors

The cannabis industry is expanding at an astounding pace, and companies competing for a share of this market face unprecedented challenges – and extraordinary opportunities. Often, we see rapidly growing cannabis companies running multi-million dollar operations on entry-level accounting software and spreadsheets. Lots of spreadsheets.

Simplified solutions (like QuickBooks or seed-to-sale solutions) give you one-dimensional insights, then make you do the heavy lifting to get the answers you need. Disconnected, incomplete applications rob the organization of the visibility needed to sustain growth, expansion, and profitability.

Don’t let the wrong cannabis software hold you back.

Embrace a clearer way to run your business. As your cannabis business grows and seizes great opportunities, how you handle your systems and tasks affects every part of what you do – from planting to selling, tracking, maintaining compliance, and making sure orders are fulfilled.

Introducing SilverLeaf, the leading cannabis solution built to integrate every function of your business, from seed to sale, tracking to compliance, procurement, fulfillment and finance, built on top of the best-in-class ERP, Microsoft Dynamics 365 Business Central.

Manage Your Entire Business in One Place

We’ve spent three decades implementing and configuring ERP for industry leaders and value Microsoft Dynamics 365 Business Central as the foundation of SilverLeaf because it was designed for manufacturers and distributors.

D365 Business Central (BC) also gives our team the flexibility to configure extensible solutions that are industry-specific for cannabis growers, yet manageable for a lean IT team.

Comprehensive Features

- Track costs associated with cultivation

- Predict yield by location and strain, with seasonality

- Complete plant tracking by tag throughout your facility

- Destruction Tracking

- Label Printing

- Track Mother Plants

SilverLeaf enables your compliance strategy, streamline for greater control, and gain real-time insight across leveled perspectives

- Built on world-class ERP platform Microsoft Dynamics Business Central

- Robust, real-time financial reporting

- Multi-Entity support

- Support of 280e strategy

- Item cost analysis

- Security and Audit Trail

- Strain management

- Recommended replenishments

- Product destruction tracking

- Label and tag printing

- Integration with State Track and Trace systems

- Track vendor and location license information

- Complete production management and scheduling

- Lot tracing with forward and back traceability

- Machine scheduling

- Track component, labor, indirect costs and variances

- Ad hoc consumption scanning

- User definable tests and measures

- Quarantine management

- Lab billing reconciliation

- COA email with order

- “Inheritance” of test results from raw materials to manufactured or assembled products

- Matrix order entry

- Visibility to inventory availability

- License management

- Sales manifest generation

- Delivery dispatch with chain of custody tracking

- Integration with wholesale distribution platforms such as LeafLink

What SilverLeaf Cannabis ERP Can Do For You

Enhance Efficiency

Maintain Regulatory Compliance

Engage in Strategic Planning

Streamline Production

Gain Insights and Visibility

Inventory & Procurement

Cultivation & Quality Controls

Sales and Delivery

Maintain Regulatory Compliance

Integrate and reconcile your cannabis growers data with state tracking systems (e.g. Metrc, BioTrackTHC, Leaf Data Systems). Support the execution of your 280e strategy. Track and maintain state and local business tax requirements for cannabis growers (sales, excise, cultivation). Utilize auditable financials, with robust tracking of system usage throughout, and support GAAP and IFRS environments.

All these necessary system integrities, process assurances, and tools are built into SilverLeaf ERP for Microsoft Dynamics 365 Business Central.

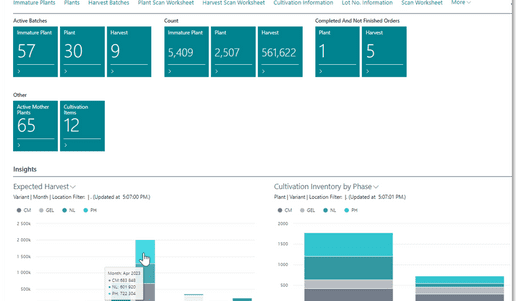

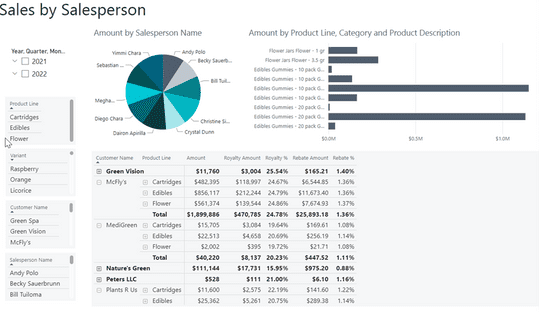

Real-Time Business Insights

With just a few clicks, effortlessly drill down into key performance indicators (KPIs) to access comprehensive details. Empower your team with instant data and streamline decision-making like never before.

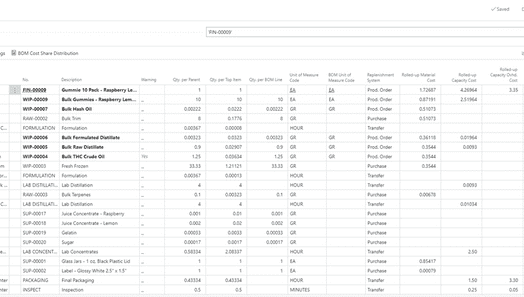

Understand the True Costs of Products

Gain the power to comprehensively monitor all costs associated with your products, encompassing raw materials, production costs, labor, and overhead. Utilizing the “Cost Shares” screen, you can access real-time insights into the projected current cost of producing each item, enabling you to make informed decisions and maintain a competitive edge in the market.

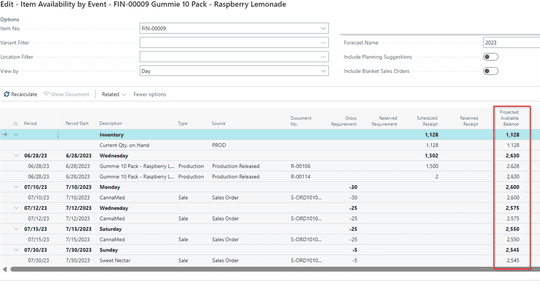

Instant Inventory Insights

Always know what your current on-hand inventory, and what you have available to sell by day, week or month. “QC Unavailable” will show you the quantity that has not yet passed lab testing. And, with each batch or tag you can see the associated lab results.

Integrate with the Microsoft Platform

This provides a sneak peak into our role center. This shows our ‘grower role center’. It is showing the expected yield by strain by period or by phase. Because SilverLeaf is built on the Microsoft Dynamics platform, SilverLeaf will integrate with popular tools such as Excel, Word, Teams, Outlook and Power BI.

Learn how DreamFields Leveraged SilverLeaf to Boost Efficiency and Process $1 Million in Revenue in One Day

DreamFields had big growth plans, and needed a technology stack with the flexibility and comprehensive features to support them. With SilverLeaf, DreamFields now has a single unfied login and consolidated ERP platform – saving them time and money. Month-end close is much easier and reporting is more accurate.

Cannabis Growers and Processors

Solution Benefits

Why Velosio for Your Cannabis Grower and Processor Software Solution?

Demo Videos

Our Latest Recognitions

A Business Leaders Guide to Dynamics 365 ERP

Velosio’s Microsoft experts will weigh in throughout to share insights and best practices gleaned from years on the job. Additionally, this series examines emerging trends, product updates, and how real companies use D365 in the real-world – putting the game-changing ERP in a broader context.

Our Clients

See Why Cannabis Producers Choose SilverLeaf

Trusted by cultivators, processors, and distributors to simplify compliance, inventory management, and operations.